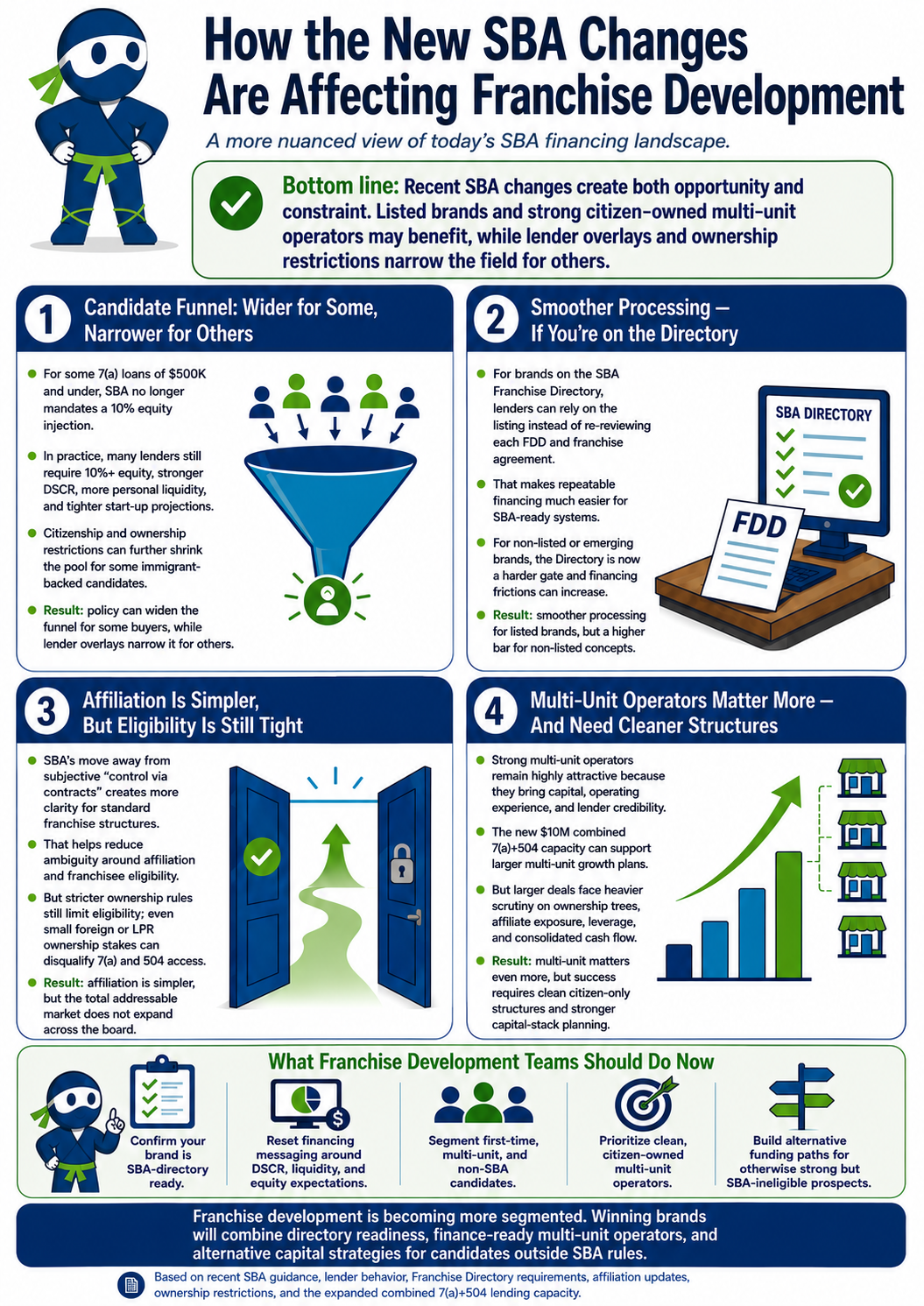

SBA Financing Changes and The Impacts on Franchise Development

Over the next 12 to 18 months, the SBA is rolling out some of the most consequential franchise financing changes in years, reshaping who qualifies for SBA-backed loans and how those loans are underwritten. For franchisors and development teams that rely on 7(a) and 504 financing to support growth, these are not minor compliance updates. They affect candidate eligibility, lender review, capital requirements, approval timelines, and ultimately how scalable a franchise model is when prospective owners need outside financing.

Changes to SBA Financing

Ownership and Eligibility

The most disruptive shift is in borrower eligibility. The SBA is moving toward a stricter standard that effectively requires SBA-backed borrowers to be wholly owned by U.S. citizens or U.S. nationals. This marks a clear break from prior policy under which Legal Permanent Residents (LPR) were generally eligible. For franchise systems, that change matters because even a relatively small ownership interest held by an ineligible person may jeopardize the borrower’s ability to qualify for SBA financing.

Recent guidance also narrows eligibility across other non-citizen categories, including DACA recipients and certain asylum-based applicants. On top of that, the SBA’s six-month “lookback” approach adds another layer of risk. The lookback rule states that if an ineligible individual held an ownership stake in the business during the prior six months, the borrower may still be deemed ineligible even after that interest has been transferred. In practical terms, this creates added friction for:

Franchise resales

Multi-entity ownership structures

Syndicated investments

Any deal where ownership has recently changed hands

As a result, franchisors, lenders, and deal advisors will need to pay much closer attention to capitalization tables, ownership history, and entity structure earlier in the development process. A franchise candidate who appears qualified operationally may still become unfinanceable if the ownership profile is too complex or does not align with the SBA’s revised standards.

Franchise Directory and Documentation

The SBA Franchise Directory has once again become a central checkpoint in franchise finance. If a brand is listed, lenders can generally rely on that designation rather than re-analyzing the franchise relationship from scratch. If a brand is not listed, however, the franchisor typically must submit its Franchise Disclosure Document (FDD) and related agreements for SBA review before the loan process can move forward in any meaningful way.

That distinction has real operational consequences. Listed brands are better positioned for repeatable financing because:

Lenders can move more quickly

Legal review is reduced

There is greater consistency across transactions

Unlisted brands, by contrast, face extra review time, more administrative coordination, and a higher likelihood that financing delays will slow openings, transfers, or broader expansion efforts. For emerging systems or brands entering new markets, Directory inclusion increasingly functions as a prerequisite rather than a back-office compliance detail.

At the same time, the SBA appears to be simplifying parts of the affiliation analysis by emphasizing ownership more than contractual control. That may reduce friction for straightforward single-unit franchise deals, but it could create more uncertainty for multi-unit operators, multi-brand groups, and private equity-backed structures that do not fit a simple ownership model. In those cases, what looks like a technical rules change can materially alter whether a deal is easy to place with an SBA lender.

Credit Standards, Fees, and Loan Structure

The financing environment is also becoming more conservative from a credit standpoint. Upfront guarantee fees have returned for many loans above $150,000 with longer terms, adding cost to already capital-intensive franchise transactions.

At the same time, the range of loans eligible for streamlined “small loan” treatment is narrowing. This means more borrowers may be pushed into fuller underwriting with additional documentation, deeper cash-flow analysis, and more lender discretion.

For franchise buyers, that translates into a higher bar on both qualification and deal economics. Lenders are placing greater emphasis on liquidity, credit profile, business projections, and the borrower’s ability to absorb uncertainty in the ramp-up period. Equity injection requirements are also reemerging more forcefully for start-ups and acquisitions, making it harder to rely on highly leveraged structures that previously helped marginal candidates get across the finish line.

Contingency reserves are another area to watch. Where a 10 percent reserve may once have been sufficient, lenders are increasingly looking for larger cushions to account for construction volatility, inflation, delayed openings, and slower-than-expected early performance. That pushes the total capital requirement higher and may shrink the pool of otherwise interested candidates who simply cannot meet the new cash demands.

Operational Impacts for Franchise Development

These policy changes do not operate in a vacuum. They are landing at a time when added complexity and staffing constraints are contributing to longer SBA review and approval cycles, including within channels that were historically more efficient. For franchise development teams, that means slower time-to-close, more fallout risk during the sales process, and a stronger need to qualify candidates on financing readiness much earlier than before.

The practical implication is that franchise systems can no longer treat financing as something that gets solved after a candidate signs. Directory status, ownership eligibility, liquidity, and structure all need to be addressed earlier in the funnel. Brands that build those checkpoints into development operations will be in a better position to preserve velocity, while those that do not may see more stalled deals, more abandoned applications, and more strain on broker and lender relationships.

There is, however, a strategic upside for brands that adapt quickly. Once a franchise system is properly positioned in the SBA Franchise Directory and its documentation is aligned with SBA expectations, lenders can process deals more consistently and franchisees may avoid repeated legal friction in each transaction. In that sense, compliance becomes more than a legal requirement; it becomes a competitive advantage that can make financing more repeatable across units, markets, and development cycles.